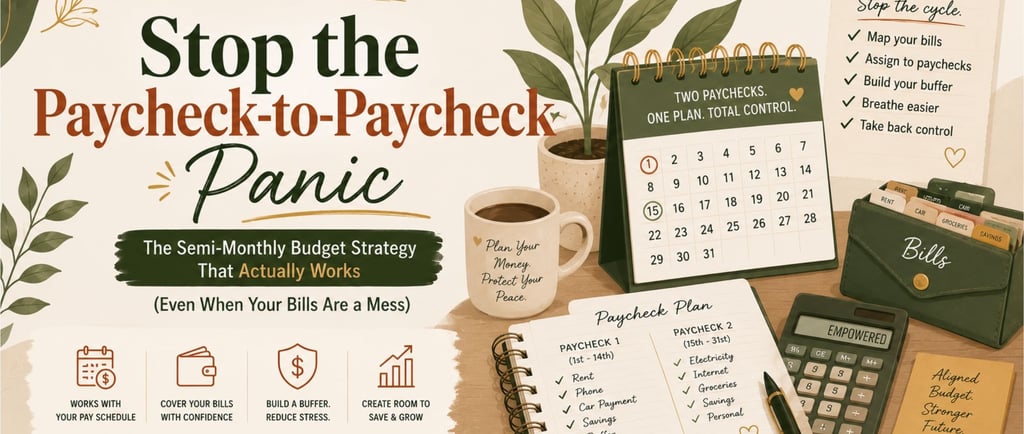

Stop the Paycheck-to-Paycheck Panic: The Semi-Monthly Budget Strategy That Actually Works (Even When Your Bills Are a Mess)

Stop the Paycheck-to-Paycheck Panic explores a simple but powerful budgeting strategy designed for women of color who are paid twice a month and constantly feel financially behind. This practical article breaks down how to assign bills to specific paychecks, organize cash flow, build a financial buffer, and reduce money stress, helping readers move from financial chaos to confidence without needing a higher income.

You get paid on the 1st and the 15th of the month, and somewhere between those two dates, financial chaos quietly takes over. The rent is due on the 1st, the car note on the 10th, the electricity bill surprises you on the 22nd, and by the time your next paycheck arrives, you are already running on fumes and prayers. You're not irresponsible; you're disorganized in a system that was never designed with your pay schedule in mind. Millions of people earning decent money still find themselves short because traditional budgeting advice was built around a single monthly paycheck, not the jagged, two-payment rhythm that many workers live with. The good news? Once you understand the structure of your cash flow, you can stop reacting to your finances and start leading them and it doesn't require a finance degree or a six-figure salary to make it happen.

Why Semi-Monthly Pay Creates a Unique Challenge

When you're paid twice a month, typically on the 1st and 15th (or sometimes every two weeks), you receive 24 paychecks per year. That sounds great, but here's the trap: your bills don't care what day you got paid. They're scattered across the calendar like landmines, and most people mentally pool their two paychecks into one imaginary "monthly income" without ever mapping which paycheck will cover which bill.

Here's a simple example:

Monthly take-home: $3,200 (two paychecks of $1,600 each)

Rent: $900 (due 1st)

Car payment: $350 (due 10th)

Groceries: ~$300/month

Electricity: $120 (due 22nd)

Internet: $60 (due 18th)

Phone: $80 (due 5th)

Subscriptions: $40

Personal spending: ~$200

Savings goal: $150

Total: ~$2,200

On paper, you have $1,000 left over. But if your first paycheck ($1,600) has to cover rent ($900), phone ($80), and car payment ($350) — that's $1,330 gone before the 11th. You're left with $270 to survive until the 15th. No wonder it feels impossible.

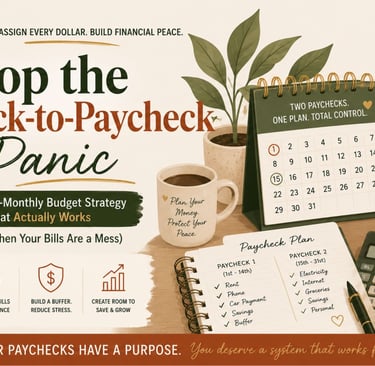

The Fix: The Two-Paycheck Assignment Method

According to "Your Money or Your Life" by Vicki Robin and Joe Dominguez in their book on personal finance, they state that the key to financial peace is alignment: matching your money's arrival with your money's purpose. The method below puts that philosophy into practice for semi-monthly earners.

Step 1: List Every Bill and Its Due Date

Write down every recurring expense and the date it's due. Be honest, include Netflix, that gym membership you keep meaning to cancel, and your weekly grocery run. Use a simple spreadsheet or even a piece of paper.

Step 2: Assign Each Bill to a Paycheck

Divide your calendar into two windows:

Paycheck 1 (1st–14th): Assign bills due between the 1st and 15th

Paycheck 2 (15th–31st): Assign bills due between the 16th and end of month

Using the example above:

Paycheck 1 ($1,600) Paycheck 2 ($1,600)

Rent: $900 Electricity: $120

Phone: $80 Internet: $60

Car: $350 Groceries: $300

Savings: $75 Subscriptions: $40

Buffer: $195 Personal: $200

Savings: $75

Buffer: $805

Suddenly, both paychecks have a job and you can clearly see where you stand.

Step 3: Shift Due Dates Where You Can

Most people don't realize that you can call your service providers and change your billing date. Credit card companies, phone carriers, and utility companies will often accommodate a request. This one phone call can rebalance your payment windows dramatically. Aligning bill due dates with pay dates is one of the simplest and most overlooked budgeting hacks available.

Step 4: Build a "Bill Buffer" Account

Open a free second checking account (try to find one with no fees). From each paycheck, transfer a set amount, even $50 or $100, into this account. This is your buffer for unexpected bills, late fees, or those months when a bill hits two days before payday. This is referred to as creating "financial breathing room," a small cushion that breaks the cycle of constant shortfalls.

Step 5: Use the Zero-Based Budget Principle

Dave Ramsey popularized this approach: give every dollar a name. After assigning all your bills and savings to each paycheck, allocate the remainder to specific spending categories: groceries, fuel, entertainment, etc., until you reach zero. This doesn't mean you spend everything; it means every dollar has a planned destination, including savings.

A Quick Reality Check: What If There's Not Enough?

If, after assigning bills, you realize Paycheck 1 simply can't cover everything assigned to it, you have three options:

Shift a bill to Paycheck 2 (call the provider)

Cut a non-essential temporarily (pause a subscription)

Increase income; even a small side gig can cover a $50–$100 gap

According to a 2023 report by Bankrate, 57% of Americans can't cover a $1,000 emergency expense, not because they earn too little, but because they lack a system. A system changes everything.

If you had to cut one bill tomorrow to free up cash, which would it be?

Budgeting on a semi-monthly paycheck isn't about deprivation; it's about direction. When you assign each paycheck a specific set of bills, you stop guessing and start knowing, and that knowledge alone is worth more than any app or spreadsheet. The feeling of "always ending up short" is almost never about not earning enough; it's about money moving without a plan, quietly disappearing into the gaps between paychecks. Once you take the time to map your income to your obligations, something powerful shifts: you move from surviving your finances to actually managing them. You deserve a budget that respects how you get paid, not one that assumes your life fits a textbook model. Now you have the tools to build exactly that.

The following are some of the resources used in preparing this article:

Bankrate. (2023). Bankrate's Annual Emergency Savings Report. Retrieved from https://www.bankrate.com

Ramsey, D. Zero-Based Budgeting. Ramsey Solutions. Retrieved from https://www.ramseysolutions.com

Robin, V., & Dominguez, J. (2018).Your Money or Your Life: 9 Steps to Transforming Your Relationship with Money and Achieving Financial Independence. Penguin Books.